In my last article, I looked back at how 2D digital printing developed in the decade of the 1990’s and discussed how 3D printing equipment manufacturers now, could apply the lessons learned then.

Even when writing it, the story felt so one-sided. It takes two to tango as they say. Equipment manufacturers would have never gone to a revenue sharing model if customers hadn’t forced them to.

So, I decided to write this article from the buyer’s side of the desk. Even though I’ve also worked for several large commercial printers and have directly bought or influenced the purchase of a considerable amount of expensive equipment, I’m guessing that by now, you must be growing tired of my rants.

So, I decided to get some perspective from my old friend and customer, Dale Maloney.

Back in the day, Dale was in charge of Relizon’s fleet of digital presses. When I was working for Xerox, he was my customer. I was referring to him specifically when, in my last article, I wrote:

Big players said, “if you want to do business with us, we need to share revenue.” They wanted a fixed price per page based on the volume they managed. If new equipment was introduced, they wanted to be upgraded automatically.![]()

Originally a division of Dayton, OH based Reynolds and Reynolds, Relizon was formed when the company split its automotive and print operations. At its peak, Relizon had nearly a billion in annual revenue and derived much of it from document management, billing and relationship marketing services. It was also one hell of a big printer.

Volume + Competition = Opportunity

We met for lunch and I asked Dale about his motivation for moving to a rev-share model. He told me he didn’t have any choice. His management team told him to upgrade all of their equipment and when he asked for a budget, they told him there was none. So he started thinking about what assets he did have, and volume seemed most obvious. At that time, Relizon’s shops were routinely printing over 100 million pages per month.

He was searching for a way to meet the demands of his bosses and found inspiration in pay phones, of all things. Back then, the Bell companies would put pay phones in high traffic areas. If they got significant usage they’d add another and another and so on. The property owner didn’t pay for the phone, they supplied the users. He wondered if a similar model could work in print.

He was searching for a way to meet the demands of his bosses and found inspiration in pay phones, of all things. Back then, the Bell companies would put pay phones in high traffic areas. If they got significant usage they’d add another and another and so on. The property owner didn’t pay for the phone, they supplied the users. He wondered if a similar model could work in print.

When he brought the idea to Xerox, our management team nearly went through the roof. In those days, our compensation plans and budgets were based on “installs.” When Xerox sold a piece of equipment, they would immediately record the entire value of the sale, and the service and anything else that could be bundled in. A $250,000 machine might be worth a million or more in installed revenue.

It was literally all about the install. There were even times when they would “install” a machine on a customer’s dock or in some warehouse. All they had to do is power it up and print one page. After that, it was considered a sale and five years worth of annuity came rushing forward.

While Dale’s plan would generate a lot of monthly revenue it wouldn’t yield installs. The only way to accomplish what he wanted was to put Relizon on a rental agreement, and that sucked for Xerox.

So why did they do it? Competition.

Dale had already met with Canon and convinced them to propose a rental agreement. They had nothing to lose and everything to gain. If they won the business they would have a contract worth hundreds of thousands of dollars each month. With that on the table, Xerox really had no choice. If they didn’t play ball they’d be on the outside looking in for a very long time.

That’s a really big lesson for 3D printing service bureaus. Many times suppliers will say they can’t or won’t offer a deal and usually those reasons have to do with their own internal paradigms. But a competitive threat is like a solvent that breaks those down. The key is in the setup.

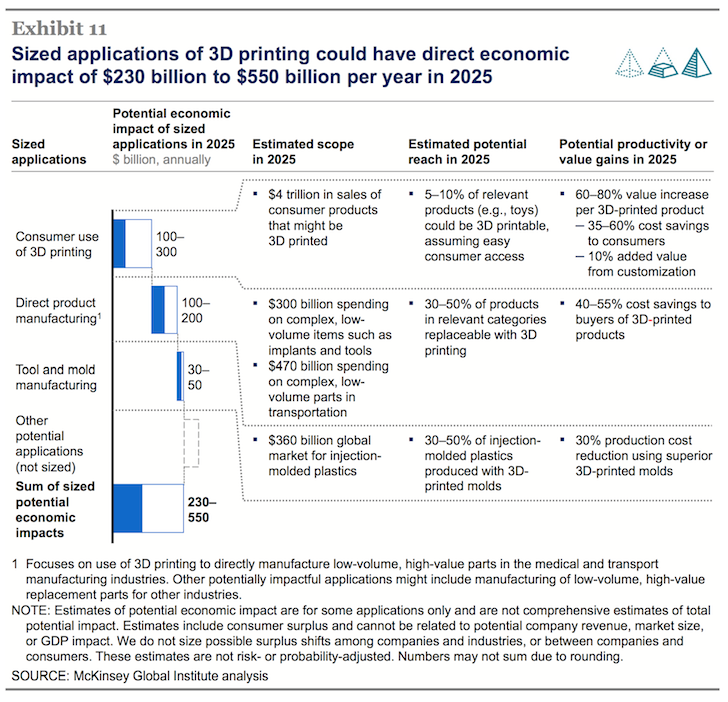

First, you have to build volume. Personally, I think much of that in 3D will come from end-use products. It seems McKinsey agrees, noting that consumer use of 3D printing could have an economic impact of up to $300 billion 2025. Direct product manufacturing could contribute another $200 billion.

In their report, they go on to say that:

As of 2011, only about 25 percent of the additive-manufacturing market involved the direct manufacture of end products. With a 60 percent annual growth rate, however, that is the industry’s fastest-growing segment. As costs continue to fall and the capabilities of 3D printers increase, the range of parts that can be economically manufactured using additive techniques will broaden dramatically.

But to grow volume you need equipment and/or capacity. When buying equipment, it’s important to have a strategy and not get trapped in an endless upgrade cycle.

“The same risk exists in 3D that I faced with 2D,” Dale told me. “The technology and its capabilities will change at a rate faster than the economic model to pay for it. Halfway through the cycle or less, a new generation of equipment will emerge that’s more productive and has more capabilities, making your remaining economic payback for the last generation of equipment uncompetitive and possibly toxic to the business.”

He went on to remind me of the horrible job some companies did of managing their equipment leases. They would forget about them (hard to imagine, I know) and end up auto-renewing leases on machines with dollar buyouts. So instead of simply exercising the purchase option, they would pay thousands of dollars each month to continue leasing.

Second, you must resist the urge to become a one-vendor shop. You have to create a competitive environment. That’s becoming easier. New players with big resources are flooding into the market. In fact, just this week, Japanese 2D printer manufacturer, Mimaki, announced their intention to join the fray. The more the better from a service bureau’s standpoint.![]()

But remember that while competition makes a rev-share model possible, it also breeds all kinds of silliness. First you can expect equipment providers to compete directly against you. Even though they should know better, Mimaki’s plan is to begin by “offering 3D printing as a service. This beta-phase will allow the company to make sure their technology works correctly before they officially begin selling their printers to other companies.” Really?

You can also expect them to try to put a printer on every desk. Even though the lion’s share of volume was a better fit for departmental or production devices, at one point, desktop printers littered the enterprise. They became so cheap that nearly anyone could order one (or more). In fact Dale reminded me of circumstances where people would buy two of the exact model, take one home, and then bilk their employer for the supplies for their home machine.

Which is really interesting in light of a recent Northrop Grumman Survey from Robo 3D. In it they found that 85% of engineers would do more prototyping if they had a 3D printer at their disposal. The CEO of Robo 3D, Braydon Moreno interpreted that to mean that, “The old ways of sending parts off to expensive industrial machines within companies is archaic. Engineers should be able to create and recreate on their desktop quickly with the accessibility of a personal 3D printer.”

In the case of 2D printing, that strategy was often 10X more expensive than printing the same job on an “expensive industrial machine.” Not only because the price per print is considerably higher, but also because of soft costs including personal use, and worse.

Dale reminded me of the story of one hospital system whose purchasing manager walked into a Porsche dealership and tried to pay with cash. The sales rep got a bit suspicious that a guy making $30K a year had $60K sitting there in a briefcase. They did some digging and it turns out he had a deal with the hospital’s office supply rep to walk around the corner and fill his trunk with the supplies his employer had paid for. He would turn around and sell them on Craigslist. That particular purchasing manager might still be in jail.

Note that I’m not suggesting that in today’s world, engineers shouldn’t have access to 3D printing – only that for the above reasons giving them all desktop 3D printers probably isn’t the best strategy. It’s so much easier, and in the long run less expensive, to let them order online.

The lesson for service bureaus is this. Focus on your workflow, right now. Make it easier for your customers to order online, drive transaction cost out of your system, provide clients with data about their usage, and give them insight about how they can leverage your services more effectively. That will allow you to grow your volume and keep competition at bay.

As Dale put it, “3D printing right now is about capturing the first position. But as it expands, the critical mass will require improvements in workflow, manufacturing processes, and distribution with the goals of improving productivity, efficiency and ease of use.”

Yessir.

Once you’ve got a well-oiled machine that’s driving significant volume, you can effectively pit competing equipment suppliers against one another to build a rev-share model that’s based on mutual benefit.

And keep in mind that If you don’t, someone like Dale Maloney will.

So what’s he up to these days, you ask? Well, Dale’s currently helping one of America’s largest financial services companies optimize their workflow and strategically outsource their print. After that, he swears he is going to retire…unless I can convince him to do it all over again in with 3D printing. Can you imagine? The two of us old war horses riding off into another battle? Now that would be epic.